Financial institutions are shifting away from reactive AML enforcement. The way financial institutions identify, stop, and deal with financial crime is being drastically changed by artificial intelligence. What was originally a helpful tool is now playing a major role in contemporary compliance initiatives. The speed and volume of quick payments, as well as sophisticated criminal strategies, are too much for outdated, rules-based systems to handle.

The application of AI for AML and compliance procedures is about to enter a new evolutionary stage in the business. Although transaction monitoring is still the cornerstone, AI is changing how AML compliance works. AI-driven monitoring assesses record of transactions, ambient risk metrics, and behavioral trends in real time rather than depending on set thresholds. Sophisticated AI systems that can foresee illegal activities and offer profound context-specific analyses before any transaction report, are replacing basic pattern recognition. They can examine ‘countless’ variables in real time compared to manual approaches. They have the potential to ease the process of distinguishing between a professional money launderer and a legitimate business owner radically. Replacing individuals is not the goal or the chased outcome here. The emergence of deepfakes and AI-powered schemes in financial crime serves as a clear reminder that technology has two sides. Adopting new technology is only one aspect of this change. It involves compliance teams actively influencing the integration of AI into risk management procedures. Giving compliance specialists the resources they require to concentrate on real threats rather than tedious data entry is the goal.

In order to combat financial crime, the majority of organizations currently have ongoing initiatives or are in the process of implementing AI. Static, rule-based systems are a major component of conventional AML solutions and these methods are still essential. They are just not able to meet the demands of modern compliance. Efficiency is not the only factor driving this change. Strict guidelines are being established by new laws for AI. EU AI Act, which is effective in 2026 is the first about this shift. These regulations mandate that AI systems be understandable and transparent. It will not be a surprise to see similar acts in the AML compliance world.

Today what is needed in AML complience is to improve bank staff productivity, maintain efficiency in costs, satisfy authorities and upper management, and continue to be customer-focused. The scalable technology that can provide these and reliably differentiate between complicated financial crimes and normal customer behavior at scale is advanced artificial intelligence. To keep your team ahead of emerging risks , agentic AI layers are capable of interpreting enormous volumes of data and performing hypothetical scenarios on their own.

The following topics are going to be covered in this article;

- What Is AI in AML Compliance? A Plain-Language Overview

- The Evolution: From Rules to Intelligence

- Where AI Is Applied Across the AML Lifecycle

- The Numbers: What AI Actually Delivers

- What Regulators Think About AI in AML

- AI in AML: What's Hype vs What's Real

- How to Get Started: A Practical Framework

1. What Is AI in AML Compliance? A Plain-Language Overview

AI in compliance is the application of machine learning (ML), natural language processing (NLP), and predictive modeling for better risk evaluation, identifying fraudulent transactions, and compliance oversight. For a Money Laundering Reporting Officer (MLRO), artificial intelligence (AI) represents an upgrade from static rules to learning systems. Conventional AML systems function similarly to a strict set of guidelines: "If a transaction is over $10,000, flag it." This was effective decades ago, but now it results in a deluge of false alarms that squander the time of your crew. AI doesn't merely follow a script, when examining your data. It identifies typical behavioral patterns, and notifies you when something genuinely sticks out as suspiciously incoherent. In essence, it learns what good looks like in order to identify bad more precisely.

AML Compliance solutions that are powered by artificial intelligence promise to be more proactive and effective. The method benefited is actively acquiring knowledge and adjusting to new potential risks, as opposed to depending on manual inspections and rule-based systems. There is a wide variety of technologies and approach methods that address various compliance issues. The ability to learn, produce, or act autonomously defines the stage history and the methods in artificial intelligence.

- Machine Learning (ML): Machine Learning is the foundation and its focus is the algorithms that learn patterns from data, and then to make predictions or classifications. The engine that examines millions of transactions to uncover hidden connections between accounts is called machine learning, or "The Pattern Finder." It finds "outliers" that a MLRO staff or a straightforward rule would miss. Natural Language Processing (NLP) contributes to the system of reading. It can scan news articles, corporate filings, and sanctions lists in dozens of languages to find adverse media that a human might miss.

- Generative AI (GenAI): Generative AI stands for specialized ML models like LLMs which are highly popular in the AI race. They create new text, images, code as content, as a response to a prompt. The Writer, or Generative AI, acts as a digital assistant. It can create a draft Suspicious Activity Report (SAR) narrative for your team to review after reading thousands of pages of news items or company filings.

- Agentic AI: The most recent change is Agentic AI. They are advanced systems that are based on AI, often GenAI. Their focus is to autonomously plan, take action, use tools, and achieve multi-step goals with minimal human oversight. These digital workers are capable of carrying out multi-step activities. Before a human even sits down at their workstation, an AI agent, for instance, can identify an alert, collect the customer's ID, examine their social media footprint, and compile the entire inquiry into a folder. In order for auditors and model risk teams to determine why a client is rated high, medium, or low, AI-enhanced risk profiling should provide visible, explicable risk scores. Agentic AI should be adapted in a way that shows AI isn't operating independently in ways that can't be audited or explained. Instead of being truly adaptive, goal-driven intelligence, the majority of technologies labeled as agents today are actually process automations. Explainability and safeguards should take precedence. Agentic capabilities will have to demonstrate that judgments, actions, and suggestions continue to be transparent, traceable, and under human supervision.

Why Is This Happening Now? We have reached a tipping point as some major factors came together:

- Data availability: The high amount of exponentially raising data finally given AI systems a meaning of existence. As data gets high-quality and structured, AI systems will keep delivering better outcomes and work effectively. The global adoption of data keeping standards is another factor at this point.

- Computing Power: Modern systems can now process millions of transactions per second. This fuels AI systems with better and deeper learning opportunities, and more accurate analysis power.

- Regulatory Pressure: Regulators like FinCEN and the European Commission have moved the goalposts. The EU AI Act (August 2026) requires AI systems to be transparent and explainable.

- Escalating Crime: Criminals are now using "Crime-as-a-Service" platforms and AI-generated identities. Rule-based systems simply cannot keep up with an enemy that changes its tactics every few hours. Regulatory encouragement to encounter these methods with AI itself, is another factor here as well.

2. The Evolution: From Rules to Intelligence

It has taken time for automated intelligence to replace manual oversight. Every stage in this evolutionary process resolves the shortcomings of the one before it. The compliance industry is currently in the middle of a massive upgrade cycle. Although autonomous agents are the industry's desired destination today, the majority of financial institutions are really still figuring out how to move from Generation 1 to Generation 2.

A technological improvement and adaptation was fueled in time. The reasons were due to regulatory pressure, exponentially enlarging data volumes, and new tactics invented for money laundering. AI came in support with automation, cloud computing, and modular designs.

Timeline format showing four generations:

- 1990s-2000s: Rule-based systems with fixed thresholds (if transaction > $10K, flag). Rule-based transaction monitoring systems from the 2000s had very high false positives, with the majority of warnings being noise. Alerts were delayed and reactive in nature. They appeared only after damage had been done. Rigid rules, and little flexibility resulted in many blind spots, including disjointed teams, systems, and tools. New laundering tactics couldn't be accommodated by static rule sets. Growing volumes were too much for manual reviews to handle.

- 2010s: Machine learning, supervised models trained on historical SARs to score alerts. Businesses started utilizing supervised machine learning as data storage became more affordable. Systems were trained on thousands of prior Suspicious Activity Reports (SARs) rather than just rules. The system was trained to score alarms according to how closely they resembled previous incidents. Although it was still reactive, this assisted teams in setting priorities for their work. Because it hadn't yet seen it in the training data, the model frequently overlooked novel laundering techniques developed by criminals. Automation and combined compliance systems include features like workflow connection, CDD/KYC checks, computerized report generation, and basic risk assessment.

- 2020-2023: GenAI/NLP, natural language processing for adverse media screening, document analysis, SAR narrative drafting. Early generative AI and natural language processing (NLP) were introduced during this time. For the first time, machines were able to construct the narrative sections of SARs, "read" adverse media, and scan through thousands of pages of beneficial ownership paperwork. Investigators are not a data entry clerk at this point. They function more like an editor, as an office worker is still needed to initiate the stages of the procedure with these tools.

- 2024+: Agentic AI autonomous agents that investigate, decide, and act with human oversight. Advanced AI systems and computing power feeded worldwide legislative versatility, explainable models, practical and efficient settings, real-time monitoring, and customizable systems. We are about to reach the era of Agentic AI or Digital Workers. These are self-governing agents that don't wait for an inquiry from a human. The agent can freely choose to obtain a credit report, review sanctions lists, and examine transaction history for the previous six months when an alarm is triggered. After that, it compiles its results into a pre-investigated file. Before the officer begins to analyze the paper, the agent does the heavy lifting. There is a trend toward multi-agent systems, in which many AI agents collaborate in a single network for tasks including pattern recognition, reporting, and risk assessment.

Each generation builds on the previous. In actuality, many financial institutions are still using Generation 1 or 2 systems, despite the availability of technology to achieve Generation 4. Legacy databases that don't communicate with one another frequently cause the laggards to lag behind.

3. Where AI Is Applied Across the AML Lifecycle

AI modifies the flow of data through all phases of compliance, rather than merely superimposing itself on top of your current procedure. The objective is to establish a closed loop in which each phase influences the subsequent one. This is how it seems in real life:

(a) Customer onboarding, automated CDD, document verification, risk scoring : Although they are required compliance procedures in financial institutions, Know Your Customer (KYC) and Customer Due Diligence (CDD) are frequently cumbersome and ineffective. AI improves and automates these procedures by obtaining and confirming client information from many sources. AI-based risk profiling identifies high-risk people and organizations. Additionally, it generates an initial risk score in a matter of seconds by pulling data from dozens of external sources.

Document verification, including identity verification, is simplified with biometrics and AI-powered face recognition. Identity verification's (IDV) heavy lifting is handled by AI. During the selfie-and-ID procedure, AI models look for liveness or deepfakes. AI-driven identity verification systems speed up onboarding and guarantee that companies adhere to changing KYC laws without requiring a lot of manual involvement.

Compliance officers examine "high-risk" candidates or situations in which the AI indicates that a document may have been altered but is unable to identify the precise sort of fraud. Customers with intricate corporate structures or those from high-risk nations are handled by compliance officials. They are included in the FATF gray list, and are referred to as "edge cases".

Sanction Scanner KYB and KYC solutions make sure you don't unintentionally establish a relationship with a high-risk business by using real-time APIs to instantly verify entities and individuals against worldwide databases.

(b) Sanctions/PEP and adverse media screening, NLP name matching, contextual disambiguation, automated list updates : Natural Language Processing (NLP) excels in this situation. AI recognizes context rather than merely searching for a precise name match. It helps contextual disambiguation, and is able to distinguish between "John Smith" the local baker and "John Smith" the politician. Additionally, it searches for unfavorable reports, adverse media, that haven't yet made it onto official listings by scanning news in different languages. It guarantees Automated List Updates, which incorporate fresh information from international regulators every few minutes.

The decision on a potential match must be made by a human. A person determines if the risk is acceptable under the firm's policy, even though AI supplies the evidence. They manage the "True Match" vs. "False Positive" decision-making process for intricate matches that need specialized expertise or jurisdictional comprehension.

Sanction Scanner offers real-time access to more than 3,000 global sanction, PEP listings and adverse media. The database is updated every 15 minutes. The technology employs fuzzy matching to identify typos and intentional name changes that criminals use to conceal themselves.

(c) Transaction monitoring, behavioral baselines, anomaly detection, false positive reduction.

Instead of using strict if-then rules, AI creates a behavioral baseline for each client. It employs anomaly detection to identify patterns like structuring or smurfing. They are statistically odd but do not reach a particular financial threshold. The AI detects an abnormality if a student who typically spends $500 per month unexpectedly obtains $50,000 from a cryptocurrency exchange. By disregarding normal, yet valuable business activities, these systems reduce false positives up to 70%.

Human touch adjusts the AI models to make sure the "risk appetite" aligns with the company's policy and look into the alarms that the AI has verified as truly "anomalous." Investigators consider the "why." AI says "this is weird," but a human evaluates whether it appears to be money laundering or merely a one-time inheritance.

Boost your compliance procedure and cut down on false positives with the Sanction Scanner Transaction Monitoring tool, where more than 800 companies are redefining compliance and transaction security. Sanction Scanner keeps an eye on all of your customers' transactions in order to identify any suspicious ones. If the software finds a questionable transaction, it halts the transaction and records it for further examination. Sanction Scanner is simple to incorporate into your app via an API. The rule-writing function allows you to build scenarios and specify rules. It will reduce your burden, let you concentrate on the right signals, and reduce false positive alarms.

(d) Alert investigation, automated evidence gathering, case summarization, risk assessment:

The AI retrieves the customer's recent history, news, and associated party data as part of Automated Evidence Gathering when an alarm goes off. The customer's LinkedIn profile, recent news, and bank statements over the previous six months is collected when an alert is set off. After that, it generates a Case Summarization, condensed into a brief for the investigator. The investigator now has an updated Risk Assessment and a "ready-to-read" brief.

The human part here is to make the "judgment call." After reviewing the evidence obtained by AI, they determine whether the case should be closed or escalated.

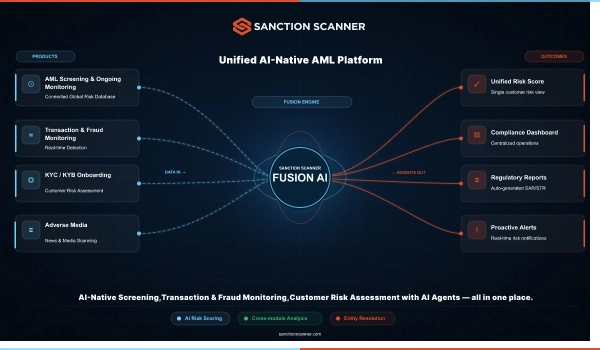

Sanction Scanner's AI-driven platform, Fusion, unifies transaction monitoring, name screening, fraud monitoring, and customer risk assessment in one platform so your team always sees the complete picture. The integrated case management dashboard allows all the data to be in one location and is consolidated for a faster final decision. Your team may see everything they require in a single view rather than having to switch between five different browser tabs.

(e) SAR filing, narrative generation, regulatory field population, quality assurance:

The narrative component of a Suspicious Activity Report (SAR) is now typically written using generative AI. It takes the facts of the case and writes a clear, professional summary that meets FinCEN or local regulator standards.

In transaction monitoring, generative AI is gaining commonplace, especially when it comes to creating SAR narratives that meet the demands of law enforcement. Generative AI is being applied to help with investigations after an alarm and create draft narratives for Suspicious Activity Reports (SARs). To standardize the quality of your documentation, and take important risk indicators out of big data sets, are also achieved with the help of AI.

AI generates structured drafts that are examined and verified, as opposed to investigators creating reports from the ground up. This changes the productivity model. A human must review each SAR. You cannot "auto-file" a SAR without having someone verify its veracity.

Sanction Scanner's platform features auto-generated SAR/STR capabilities. By automating the data input components of regulatory reporting, the Sanction Scanner software maintains consistency in your files and lowers the possibility of basic clerical errors. This ensures that the technical data required by regulators is perfectly formatted.

(f) Ongoing monitoring, pKYC, risk score recalculation, trigger-based review: This is the transition to pKYC, or perpetual KYC. The AI keeps an eye on data around-the-clock rather than waiting for a yearly refresh. The moment a customer's status changes, such as when they become a PEP, it recalculates their risk score. This is known as "event-driven" compliance. This only starts a Trigger-Based Review in response to significant events.

The "triggers" are defined by humans, who determine what particular life events or financial shifts should compel them to reconsider the connection.

Sanction Scanner's Ongoing Monitoring service re-scans your whole database daily against updated lists. You can switch from "periodic" to "continuous" compliance by instantly receiving an alert on your dashboard whenever a customer's risk profile changes.

4. The Numbers: What AI Actually Delivers

When a transaction or customer sets off an alarm that turns out to be valid behavior after further examination. This is false positive in AML screening and these can account for more than 90% of all warnings generated in conventional rule-based systems. Although the warning was a positive signal, it was false as there was no real suspicious activity. Elevated rates of false positives lead to a series of issues throughout the compliance function. Instead of concentrating on real risks that exist, agents spend their working hours addressing valid alerts.

According to studies, AI-powered AML programs achieve faster detection times than institutions that use traditional approaches. The metrics on data-driven approaches are increasingly promising. False positive reduction is up to 60-80% in time. Investigation speed doubles with 50% time savings. Despite the very high expenditures on compliance, Interpol considers that just 2% of worldwide financial crime movements are caught.

McKinsey 2024 KYC/AML Benchmark study revealed that a set of leading North American, Europe and Asian-Pacific banks, typically, banks devote 10 to 15 percent of their overall full-time employees to KYC/AML. Teams squander a great deal of time on manual labor. Data reconciliation, document collection, and routine alert processing take up important time for compliance staff. Meanwhile clients lament tedious interactions and cumbersome procedures. Data resources are dispersed and data sets are not standardized. This results in automation rates being typically poor.

A significant shift in the possible influence of AI is represented by agentic AI. Although gen AI and analytical AI increase the efficacy and efficiency of compliance, they frequently do not result in large-scale financial gains. Effectiveness and efficiency are not essentially altered by this according to Mckinsey experience.

According to Mckinsey experience the productivity improvement can be substantial, ranging from 200 to 2,000 percent with Agentic AI. According to research, a single human supervisor can now oversee 20 or more AI agents operating simultaneously. Small teams may manage the burden of much larger departments without adding more employees thanks to this force multiplier effect. Additionally, banks observe a significant improvement in output quality and consistency.

The yearly global cost of financial crime compliance has topped $180 billion. The major reason for this much high expenditure is significant part to labor-intensive manual assessments and the increasing complexity of sanctions.

75% of companies are already using AI for AML and 10% of businesses intend to employ artificial intelligence (AI) during the next three years, according to the Bank of England. This is a major increase from around the number of 53% in 2022. The AI adoption, Agentic AI in particular, is expected to reduce the $180B+ global annual compliance burden, as it is one of main driving forces of the search for solutions in efficient, reliable outcomes for less cost in the AML world.

5. What Regulators Think About AI in AML

As of today, there isn't a uniform, legally binding international standard for AI legislation. Regional or international guidelines are being developed by a number of governments and intergovernmental organizations. Other countries are less inclined to do so, especially those with weaker capacity and restricted regulatory authority. There isn't yet a comprehensive framework for incorporating AI into a larger regulatory framework.

Regulators are no longer merely spectators. The worldwide consensus has changed as they are taking steps to encourage its use in order to reduce the detection gap. Transparency and explainability are non-negotiable requirements, though.The top lesson is very clear: you have to be able to demonstrate your work if you utilize AI to make a choice about a consumer.

FATF encourages AI with explainability requirements. The substantial potential of AI and machine learning to assist Financial Intelligence FIUs, supervisors, and other law enforcement agencies was noted in the FATF's 2021 study, "Opportunities and Challenges of New Technologies for AML/CFT."

With regard to new technologies, the FATF has taken a broad and inclusive stance with FATF Recommendation 15. It mandates that reporting entities recognize and evaluate the risks connected to new services. This strategy offers a solid basis for future cooperation as AI develops, assisting nations and stakeholders in investigating how technologies like deepfakes and autonomous agents generate new vulnerabilities and how these risks may be successfully controlled by utilizing AI's advantages.

In its "Horizon Scan: AI and Deepfakes" research, the FATF highlights how deepfake and artificial intelligence technologies are drastically altering the financial crime scene. With an emphasis on AML/CFT/CPF compliance, the research examines the potential and hazards for financial institutions.

There is currently no AI-specific financial regulation or legislation in the UK. The Financial Conduct Authority (FCA) and the Bank of England, are the UK's two financial services regulators. They rely on the current framework to monitor the use of AI in finance.

FCA supports innovation with guardrails. The Financial Conduct Authority (FCA) in the UK is adopting a cautious yet pro-innovation stance. A Supercharged Sandbox where businesses can test AI-driven AML solutions using fake data is described in their 2026/27 work program. Although they have reaffirmed that the Senior Managers and Certification Regime (SMCR) applies to AI, they encourage businesses to employ AI to identify highest harm criminals more quickly. To put it another way, a human officer is still legally accountable for the choices made by the company's algorithms.

The EU AI Act, which goes into full effect on August 2, 2026, is a major regulatory development of the year. AI-powered credit scoring and transaction monitoring are categorized as high-risk use cases under this rule. By this summer, your AI systems must adhere to stringent requirements if your company works in the EU. These requirements include Documented Risk Management, human supervision, and the data quality and trust.

The AI's training data should be impartial and up to date. A transparent record of how you handle the decisions made by the AI is required. A simple kill switch should let a human take control of the machine. EU database registration is needed for some AI features. Not being specific to AML procedures, it is especially for any critical decision making processes.

As requirements for responsible AI deployment, the FATF, OCC, FCA all emphasize verified supervision by humans, transparent practices, and user requisite competence. Models created especially for investigative workflows, network detection, and sanctions screening are significantly more suitable and can offer the auditability needed for compliance judgments.

FinCEN's AML Act modernization explicitly endorses advanced analytics. Early in 2026, the AML Act's modernization in the US hit a significant turning point. The use of "high-performance data processing" and advanced analytics to detect illegal networks has been explicitly authorized by FinCEN. Currently, they are more concerned with making AML systems "effective and risk-based" than merely technically compliant. They also increased their internal usage of AI to sort through millions of SARs by March 2026. The indication is that they anticipate financial institutions to follow a similar route.

The key message from regulators are pro-ai adoption but demand transparency, explainability, and human oversight. Explainability cannot be compromised. Regulators are against black-box decisioning, not AI per se. Use AI to demonstrate how you arrived at the solution. Predictive complexity is no longer as important as transparency and evidence provenance.

6. AI in AML: What's Hype vs What's Real

What AI brought real to the AML field is high false positive reduction, faster investigations, better name matching, and automated data gathering. The hype is, 'fully autonomous compliance,' 'zero false positives,' 'replace your compliance team.'

AI has completely changed how we identify and control the risks associated with financial crime. In a matter of seconds, anomaly flagging and transaction scanning are completed, revealing patterns that human investigators could never possibly discover. However, the idea that AI is a self-sufficient answer that can take the place of human understanding is highly exaggerated, if not potentially deceptive. In the rush to adopt new technology, it is easy to get lost in marketing buzzwords.

As we navigate through the AI days, it is vital for compliance leaders to distinguish between the tools that actually work and the oversized claims that often lead to regulatory headaches. A large portion of today's "AI" is still built on rule-based systems, which are elevated versions of expert systems from earlier eras. A contextual environment is a crucial element which these aforementioned tools do not come with. Machine learning, natural language processing involvement does not change this fact.

The Reality: What AI Is Actually Doing Today

- Massive false positive reduction. This is the most tangible benefit. By using machine learning to understand "normal" customer behavior, firms are realistically seeing 60-80% fewer irrelevant alerts.

- Accelerated investigations. AI doesn't make the final decision, but it does the homework. By automating the gathering of news, corporate registries, and transaction history, it reduces the time spent on a single case by roughly 50%.

- Superior name matching. Moving beyond simple fuzzy matching, AI now uses contextual disambiguation to understand that two people with the same name are different individuals based on their age, location, or associates.

- Automated data gathering. Instead of an analyst manually checking five different databases, AI agents pull that data in seconds, creating a pre-investigated file.

The Hype: Claims to Be Wary Of

- Zero false positives is a myth. Because criminal behavior adapts to new technology and data is rarely perfect, a zero rate would likely mean the system is tuned too low and is missing actual crime.

- Fully autonomous compliance is not the reality at the current stage of AML regulations. Regulators, specifically under the EU AI Act and FATF guideline, demand human accountability. A system that makes a final legal decision like exiting a client without human oversight is a massive regulatory risk.

- Replacing your compliance team is just a slogan for now. AI is not a replacement for human intuition in the current situation. It is a tool that removes the drudge work so your highly skilled analysts can focus on the 2% of activity that actually represents a threat.

Anti-money laundering laws have been implemented through paperwork and free of tech. This is another reason why the many views on AI in AML is still a hype and employment of AI is not fast enough. Actionable guidelines on the validation, auditing, and governance of AI in the context of compliance are still lacking in many jurisdictions. The regulatory uncertainty may discourage institutions from investing in AI solutions fast enough as the hype claims.

The Honest Middleground: AI augments human analysts, doesn't replace them.

The successful programs are those that view AI as a force multiplier, not a magic wand. AI augments human analysts, and doesn't replace them. Best-in-class programs combine AI efficiency with human judgment. This balanced perspective is Sanction Scanners’ differentiator from vendors making oversized claims.

Sophisticated deep-learning AI systems function as black boxes by nature. It is challenging to interpret their choices and results. The regulatory community requires financial institutions to defend and explain compliance decisions. Filing decisions of Suspicious Activity Reports ("SARs") or red flags decisions in transaction monitoring for AML compliance have to be explainable.

The Sanction Scanner differentiator in the AML sector is the human-augmented middle ground. It is augmented intelligence, not artificial intelligence alone. The philosophy avoids the hype of total autonomy in favor of a balanced, high-performance approach. Sanction Scanner provides the speed with AI utilization to filter the noise, while the Fusion Unified Case Management provides a vast view for analysis for human analysts, which always remains the final authority. By focusing on explainable AI, every decision the machine suggests can be defended in terms of sanction regulations. This prevents the black box problem and keeps your firm compliant with the transparency laws.

7. How to Get Started: A Practical Framework

Transitioning to an AI-driven AML program is a marathon. The successful firms today will avoid big bang implementations and instead follow a modular, risk-based path. For AI systems to function well, they need well-organized, high-quality input. Incomplete parameters, inaccurate identities, and diverse formatting compromise training data and lower model accuracy. AI models won't be able to provide trustworthy insights without centrally managed information. If you are ready to move from legacy rules to intelligent compliance, follow this six-step framework:

(a) Assess the current state

Where are your biggest pain points? Before buying software, identify where your team is actually losing time. Are you drowning in 5,000 false positives a month? Is your KYC onboarding taking three days instead of three minutes? One example for pain points currently stem from fragmented data. That point being, where your sanctions list doesn't talk to your transaction monitoring tool. Map your alert-to-file ratio. If your team closes 98% of alerts as no risk, that is your starting point for AI.

Finance firms must assess the effectiveness of their compliance and AML systems. Operational limitations and vulnerable connectivity points can be found by evaluating crucial components. These can be transaction monitoring mechanisms, reporting techniques, and compliance flow charts. They must determine the appropriate amount of AI deployment given their scale, complexity, and risk characteristics.

(b) Target the Highest-ROI Use Cases

Don't try to automate everything at once. Start with the low-hanging fruit where AI delivers the fastest results, which is usually false positive reduction in transaction monitoring or sanctions screening:

- Sanctions Screening: Use AI to handle name matching and contextual disambiguation, telling two people with the same name apart.

- Transaction Monitoring: Use machine learning to noise-cancel the common, safe transactions that trigger old-fashioned rules.

These areas offer the most immediate reduction in manual labor. It often frees up 30-50% of your team's capacity within the first quarter.

(c) Evaluate Your Vendors Strategically

A vendor is more than just a software provider; they are a regulatory partner. When vetting, ask:

- Is it "Explainable"? Can the system give you a reason code or a plain-English explanation for its decision?

- Is it Cloud-Native? Can it handle real-time API calls fast enough?

- What is their security posture? Look for SOC 2 Type II and ISO 27001 certifications as a baseline.

Sanction Scanner provides a sandbox-first approach. You can test our AI models against your historical data to see the exact ROI before you commit to a full rollout.

(d) Ensure regulatory readiness , explainability, audit trail, human oversight.

The EU AI Act requires any high-risk AI system to have a clear audit trail and human oversight. Ensure your chosen system logs every decision, the data used to make it, and who reviewed it. You must be able to show your work to an auditor or regulator on demand.

(e) Pilot Before Scaling

AI-driven AML systems should be implemented gradually to help control risks and improve outcomes. Businesses must implement AI systems in controlled environments with limited data sets during the early testing phases, concentrating on certain operational domains like real-time transaction monitoring while verifying system reliability and efficiency.

Don’nt replace your old system overnight. Use a parallel run strategy:

- Keep your old rules running in the background.

- Run the AI-driven system alongside it.

- Compare the results. If the AI finds a crime the rules missed (or correctly ignores a false positive the rules caught), you have your proof of concept.

(f) Monitor and Optimize

Put together the best personnel to assist in guiding the proper AI risk recognition practices and potential risk reduction solutions that AI technologies may provide. This involves going over cybersecurity and legal requirements surrounding the application of AI, as well as involving important stakeholders from all areas of the company, including information technology, risk assessment, adherence to standards, judicial, and business management.

AI is not for set and forget. Criminals change their tactics, and model drift can happen when your data shifts over time. Set tuning sessions and recalibrate your AI models. A good system should provide a feedback loop where your investigators' decisions like true match vs. false Positive, help the machine get smarter by time.